Businesses rely on competent individuals to handle complicated financial processes and ensure that operations are precise, structured, and stress-free. But before hiring a finance expert, an important question must be answered: Do you need bookkeeping or accounting? Many people assume these two terms mean the same thing. If you think so, it’s time to clear up that misunderstanding.

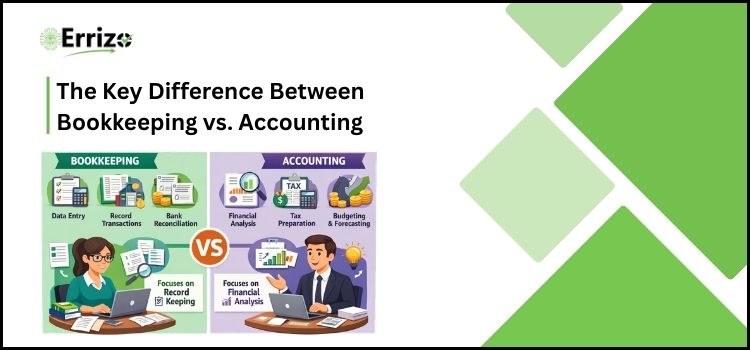

Despite their close relationship, bookkeeping and accounting have distinct roles in a company’s financial structure. Bookkeeping is the methodical recording of everyday financial events such as sales, purchases, receipts, and payments, with the goal of ensuring that each entry is accurate and up to date.

However, accounting goes a step farther. It examines and analyzes recorded data to assess financial performance, provide reports, and inform strategic decision-making. As business develops and financial rules get more complex, recognizing this distinction becomes not just useful but also necessary.

Understand the Term Bookkeeping

Bookkeeping is the systematic process of recording all financial transactions for a company in a clear, accurate, and structured manner. It entails keeping track of daily transactions such as sales, purchases, expenses, payments, and receipts. By keeping these records meticulously, a company may compile a complete and dependable set of accounts.

Proper bookkeeping ensures that no financial detail is overlooked, making it easy to track cash flow, evaluate performance, and make sound decisions. It also promotes transparency and accountability, which are necessary for auditing, tax filing, and financial reporting. Simply said, bookkeeping provides a solid basis for a company’s financial stability.

Recent Post:- Intuit’s QuickBooks the Go-To Accounting Solution

What is Accounting in the Financial Sector?

Accounting is the systematic process of evaluating, interpreting, and summarizing financial data in order to comprehend a company’s overall performance and financial situation. While bookkeeping records daily transactions, accounting converts them into useful financial reports like income statements, balance sheets, and cash flow statements.

It enables business owners, investors, and stakeholders to assess profitability, manage costs, plan budgets, and make strategic decisions. Accounting also assures compliance with financial regulations and tax laws, which promotes transparency and accountability. Accounting is critical in the financial industry for driving growth, managing risks, and ensuring long-term corporate viability.

Bookkeeping vs. Accounting: Detailed Comparison Guide

Understanding the differences between bookkeeping and accounting is critical for making smart financial decisions. To make this comparison easier, we create a detailed table comparing major elements of each method side by side. This structured overview will assist business owners and proprietors in clearly identifying their roles, perks, and distinctions, allowing them to more easily select the appropriate financial support for their business needs.

| Feature | Bookkeeping | Accounting |

| Meaning | Recording daily financial transactions in a systematic manner | Analyzing, interpreting, and summarizing financial data |

| Purpose | Maintain accurate financial records | Evaluate financial performance and support decision-making |

| Nature of Work | Administrative and Clerical | Analytical and Strategic |

| Scope | Limited to recording transactions | Broader scope including reporting, analysis and planning |

| Financial Statements | Does not prepare full financial statements | Prepares income statement, balance sheet and cash flow statement |

| Decision-Making Role | Does not directly support strategic decisions | Plays a key role in business decision-making |

| Skill Requirement | Basic accounting knowledge | Advanced accounting and financial expertise |

| Tools Used | Journals, ledgers, bookkeeping software | Financial reports, statements accounting standards |

| Regulatory Compliance | Ensure proper record maintenance | Ensure compliance with tax laws and regulations |

What are the Roles and Responsibilities of Bookkeeping

Bookkeeping is the foundation of any business’s financial structure. It guarantees that all financial transactions are accurately and consistently recorded, giving a solid foundation for accounting and decision-making. A good bookkeeper maintains the business as structured, transparent, and ready for audits and financial planning. The key roles include:

- Record Daily Transactions: Daily transactions are meticulously documented to ensure a comprehensive and accurate financial record. This guarantees that nothing is overlooked.

- Maintaining Journals and Ledgers: Transactions are recorded in journals and uploaded to ledgers to make financial data easier to manage and review.

- Managing Invoices: Bookkeepers keep track of all invoices given to clients and received from suppliers, ensuring that payments are accurately documented and follow-ups are completed on time.

- Bank Reconciliation: Comparing companies’ records to bank statements on a regular basis allows for the early detection of errors, discrepancies, or fraudulent activity.

- Payroll Management: Accurately recording employee salaries, benefits, and deductions ensures that payroll is processed on schedule and without errors.

Understand the Roles and Responsibilities of Accounting

Accounting is the strategic process of converting financial data into useful information for business choices. Accounting examines, analyzes, and publishes data to monitor performance, manage resources, and assure compliance, whereas bookkeeping simply records transactions. Accountants help businesses plan, govern, and grow by delivering reliable financial data. Here are the key roles:

- Preparing Financial Statements: Accountants prepare income statements, balance sheets, and cash flow statements that provide a concise summary of the company’s financial status.

- Analyzing Financial Data: Financial data analysis involves examining trends, costs, and revenues to discover opportunities for improvement and influence strategic decision-making.

- Budgeting and Forecasting: Accountants create budgets and forecast future financial performance to assist organizations in planning expansion and managing resources effectively.

- Tax Preparation and Compliance: Accurate tax filing and conformity to local requirements save legal penalties and maximize tax liabilities.

- Cost Control and Profit Analysis: Accountants examine expenses and revenues to suggest ways to cut costs and boost profits.

Skills and Qualifications Required for Bookkeeping and Accounting

To flourish in bookkeeping or accounting, professionals must possess a combination of technical knowledge, practical skills, and formal certifications. While bookkeepers prioritize accuracy and organization, accountants demand analytical and strategic skills. Understanding the precise skills and certifications required for each function enables firms to hire the right people and ensures that financial operations run smoothly and efficiently.

Bookkeeping Skills and Qualifications:

- Basic Accounting Knowledge: Understand the fundamental financial principles in order to accurately record transactions.

- Attention to Detail: Ensure that every sale, purchase, or payment is properly documented.

- Organizational Skills: Keep notebooks, ledgers, and invoices organized for easy tracking.

- Software Proficiency: Experience with bookkeeping software such as QuickBooks, Tally, or Zoho Books.

- Math Skills: Calculate accurately and reconcile finances without errors.

- Time Management: Manage daily transactions efficiently to ensure that records are up to date.

- Educational Requirements: A diploma or certification in bookkeeping, finance, or accounting; practical experience is preferred.

Accounting Skills and Qualifications:

- Analytical Skills: Use financial facts to assess performance and make decisions.

- Standards knowledge: Which includes an understanding of accounting concepts, tax regulations, and financial reporting obligations.

- Software Proficiency: Experienced with accounting software and Excel for reporting and analysis.

- Problem-solving Ability: Recognize financial concerns and propose solutions.

- Attention to Detail: Ensure that reports, statements, and audits are accurate.

- Formal Education: This typically includes a degree in accounting, finance, or commerce, as well as certifications such as CPA, CMA, or CA.

- Decision-Making Focus: Use data insights to help drive strategic corporate success.

Tools and Software for Bookkeeping and Accounting

In today’s high-tech landscape, bookkeeping and accounting rely significantly on specialized tools and software to efficiently manage financial data, prevent errors, and save time.

Bookkeepers utilize software to track and manage daily transactions. QuickBooks, Tally, Zoho Books, and Xero are among the most popular tools. These apps help you keep track of sales, purchases, receipts, and payments, as well as maintain ledgers, generate invoices, and reconcile bank accounts. Cloud-based bookkeeping systems can provide access from anywhere, making remote administration simple. Other tools, such as spreadsheets and calculators, are still necessary for basic computations or small businesses.

Accountants use complex technologies to evaluate and report financial data. SAP, Oracle Financials, QuickBooks, and Microsoft Excel are all useful tools for creating financial statements, budgets, tax reports, and projections. Accounting software frequently contains modules for audits, compliance, and cost analysis. Automation features save manual labor, whereas analytics dashboards provide data for informed decision-making.

Digital solutions help bookkeepers and accountants increase accuracy, save time, and streamline operations. Your organization’s size, complexity, and unique financial requirements determine the appropriate software. Efficient application of these technologies is the foundation of modern financial management.

Who Should Use Bookkeeping? Best Types of Businesses

Bookkeeping is vital for any businesses that wish to preserve correct financial records while not becoming overburdened. It is especially useful for newly established businesses or those with a simple financial structure.

- Startups and Small Businesses: New enterprises typically have fewer resources and fewer transactions. Bookkeeping ensures that all income, costs, and invoices are correctly tracked, allowing owners to make educated decisions from day one.

- Freelancers and Solopreneurs: Individuals who manage their own businesses or provide services must keep a detailed record of their revenue and expenses for tax purposes and financial transparency. Bookkeeping keeps things structured and managed.

- Retail Shops and Small E-commerce Stores: Bookkeeping may help businesses with regular sales, inventory purchases, and everyday transactions stay organized and avoid mistakes.

- Service-Based Businesses: Bookkeeping can help salons, gyms, consulting firms, and small agencies handle client payments, supplier bills, and operational expenses.

- Family-Owned or Local Businesses: Keeping correct records promotes transparency, aids audits, and facilitates expansion planning.

Who Should Invest in Professional Accounting?

Accounting is like dealing with complex finances, planning for expansion, or requiring strategic financial insights. It does more than merely record transactions; it also assists firms in making educated decisions that ensure long-term success.

- Growing Businesses and Medium Enterprises: Accounting helps growing businesses and medium-sized enterprises analyze profits, manage budgets, and plan investments.

- Businesses Needing Tax Compliance: Accounting is vital for organizations that operate in regulated industries because it assures accurate tax filing, regulatory compliance, and the avoidance of penalties.

- E-commerce and Online Businesses: Accounting assists e-commerce and online businesses with tracking performance, managing costs, and optimizing pricing strategies due to the numerous transactions, platforms, and payment channels involved.

- Companies Seeking Financial Analysis: Accounting is used by businesses to make strategic decisions about profitability, cost reduction, and resource allocation.

- Startups Seeking Investment: Entrepreneurs looking for funding or investors require adequate accounting in order to provide solid financial statements and establish credibility.

- Large businesses and corporations require accounting to ensure openness and enable audits.

Can One Person Do Both Bookkeeping and Accounting?

In small enterprises or startups, one person often handles both bookkeeping and accounting. While it is possible, efficient workload balancing needs careful planning, organization, and the correct tools. By effectively balancing both duties, a single individual may streamline the financial process, decrease errors, and ensure that the organization is financially organized and compliant from the start. Here’s how to do it:

- Begin with Accurate Bookkeeping: Ensure that all daily transactions are thoroughly documented. A robust bookkeeping foundation avoids errors and makes accounting considerably simpler.

- Use Integrated Software: Tools such as QuickBooks, Zoho Books, and Xero combine bookkeeping and accounting operations in a single platform, saving time and minimizing duplication of effort.

- Set Clear Time Blocks: Set up particular days or hours for bookkeeping (daily or weekly) and accounting responsibilities like reporting, analysis, and budgeting.

- Automate Repetitive Tasks: Like invoice generating, payment monitoring, and bank reconciling to save up time for financial research.

- Reconciliation and Review: Review financial data on a regular basis to detect problems early on. This guarantees that accounting decisions are based on reliable data.

- Use Checklists: Maintain a checklist of bookkeeping entries and accounting duties to ensure that nothing is overlooked.

- Know Your Limitations: As the company expands, the number and complexity of transactions may necessitate dividing jobs or engaging a professional accountant.

Conclusion

Bookkeeping and accounting are two separate yet complementary responsibilities. Bookkeeping keeps precise daily records, whereas accounting interprets them for strategic decision-making. Understanding their duties, utilizing the appropriate tools, and properly balancing procedures enables organizations to retain financial transparency, support growth, and make educated decisions. When properly managed, they serve as the foundation of a successful business’s financial health.